Vietnam Can Tho City 2022

EXECUTIVE SUMMARY

Rationale and Purpose

The main purpose of this assessment is to provide an objective and up-to-date diagnosis of PFM performance to inform the sub-national PFM reform agenda in CCT. The assessment will be used by the city in planning improvements to the administration of its services. It will also facilitate discussions by the city and development partners with the central government on possible changes in laws and regulations to enable better allocation of resources which would ultimately assist the city – and other SNGs more widely – in the discharge of its functions.

This PEFA assessment covers CCT, equivalent to the provincial government, which consists of both budgetary and extrabudgetary units as reflected in the PEFA Framework (PEFA Framework, February 2016 and Supplementary Guidance for Subnational PEFA Assessments, December 2016, revised October 2020 as issued by the PEFA Secretariat). The assessment takes into account information from a number of deconcentrated bodies of the central government such as the State Treasury, the Tax Department, the Customs Department, and the SAV Regional Office.

The PEFA assessment was undertaken with support from the World Bank under the framework of the SECO Trust Fund for Sub-National Public Financial Management Reform, effective April 2020. The first stage was a scoping mission in Nov - Dec 2019 to introduce the process, followed by self-assessment of CCT officials. The World Bank team reviewed and discussed the self-assessment with city officials, agreed on the evidence and its interpretation, and prepared this report in accordance with PEFA guidance. The report and its performance indicators ratings are agreed with the CCT PEFA Task Force for submission to the PEFA Secretariat and final dissemination.

The time gap between the scoping mission and main mission was due to COVID-19. Interviews and data collection used virtual communication to minimize COVID-19 disruption.

Main PFM Strengths and Weaknesses

Accurate revenue projection has become a major challenge in recent years. As a self-sufficient province, CCT no longer receives balancing transfers but only (less predictable) target transfers and (over-estimated) shared revenue (also considered as transfers in this assessment). The under-realized shared revenue is restituted by CCT’s own revenue, particularly land and lottery revenue. HLG transfers can be released without explanation about changes across years. As a result, expenditure composition varies significantly. Although its budget documentation is reasonably comprehensive, the original budget is not directly comparable to actual outturn because of the lack of economic classification in the original budget and the ‘carry-over’ practice. Timeliness is identified as a weakness in public access to fiscal information.

A medium-term debt plan is prepared, but not on the basis of cost-risk consideration. The approval of debt follows clearly defined procedures in national debt related legislation, but there is no systematic mechanism in place to identify and monitor contingent liabilities and other fiscal risks. The procedures for asset transfer or disposal and reporting are clearly established. Asset registries are in place, but assets are not recorded on fair value. Economic analysis is required for major investment project proposals but is done without clear national methodological guidance. Although the total life-cycle cost of major investment projects is projected, the recurrent cost implications are considered separately.

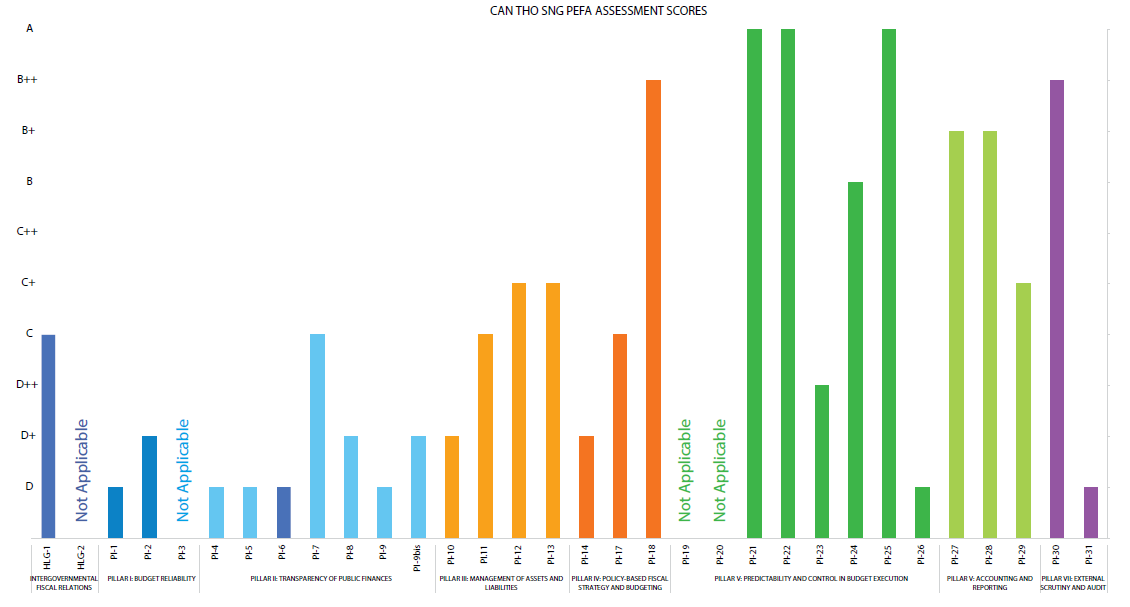

Figure 1: Summary of Can Tho SNG PEFA Assessment Rating: Indicators by Pillar

Guidance for budget preparation is provided without ceilings. The procedures for legislative budget review only include consultation with related Boards of the People’s Council and do not officially include public consultation. The People’s Council always approves the budget before the start of the FY and there are clear rules for budget adjustments by the executive. Although the medium-term perspective is recently introduced, the forecasts underlying the medium-term budget are not subject to macro-fiscal sensitivity analysis and the annual budget is not consistent with the previous year’s estimates.

CCT would benefit from reliable revenue administration, revenue sharing, and cash management, in respective deconcentrated systems operated by the central government. A Treasury Single Account (TSA) is already established for the whole nation. The State Treasury also registers commitments and verifies that all expenditure has been well controlled before payments are processed. The link between personnel records and payroll databases is not yet automated, but changes are well documented and subject to strict managerial supervision.

Procurement has improved in terms of transparency, efficiency, and effectiveness. The current control feedback function rests with the Inspection System, which focuses on compliance checks, while the internal audit function is not yet launched.

Financial data integrity processes are good, with the Treasury and Budget Management Information System (TABMIS) system in place since 2013 and regular reconciliation procedures. Accounting and reporting will be improved with the development of whole-of-government financial statements, likely to be prepared inn compliance with International Public Sector Accounting Standards (IPSAS). The current annual budget execution reports are cash-based and are externally audited regularly. The People’s Council reviews audit plans and uses the audit findings in its legislative oversight visits to selected departments and units to conduct hearings, enquiries, or debates, however, it does not scrutinize audit reports and has never issued a scrutiny report and/or its own recommendations.

Impact of PFM Performance on Budgetary and Fiscal Outcomes

Aggregate Fiscal Discipline

Aggregate fiscal discipline is poor, with weak control of the total budget, over-optimistic macroeconomic and revenue forecasts, and insufficient risk management. Macroeconomic assumptions are fixed ahead of every five year “budget stability period” without sensitivity analysis and soon become out-of-date. Analysis of fiscal risks and the fiscal impacts of policy proposals is not sufficiently robust for a credible budget. Significant variance in revenue composition is attributed to over-estimation of shared revenue and changes in tax policies by the central government. The resulting lower shared revenue is made up for by higher efforts in the collection of land revenue and lottery incomes, leading to arbitrary cut-backs during budget execution, particularly on capital expenditure.

On the positive side, fiscal discipline is supported by relatively robust internal controls of payrolls and non-salary expenditure, which result in no expenditure payment arrears. In-year budget adjustments take place with clear rules and procedures, by which social benefits, remuneration to employees, and basic operational expenses are well protected. Reporting on extrabudgetary operations is being improved with the recent introduction of the whole-of-government financial statements. The city registers its assets as required and takes a prudent stance on debt borrowing.

Strategic Allocation of Resources

Substantial variance in expenditure composition and increasing trends of expenditure being carried over from one year to the next reflect the fact that the annual budget is not a credible mirror of policies and plans. Although the medium-term perspective has been introduced recently, it is yet to help link policies, plans, and budgets as policy making, investment planning, and budgeting are carried out independently of each other. While the budget documentation satisfies all the “basic” requirements, the underlying macro-economic assumptions cannot guide the annual budget process with relatively low weight among other factors in decision making.

In accordance with policies on socialization (minimizing the role of the State in public service delivery) and autonomy (stipulating local public service responsibility for the delivery of mandates and organizational structure, personnel, and financial management), public service delivery units (PSDU) are encouraged to self-finance at least a part of their recurrent expenditure by use of service fees and other means, for example by partnering with the private sector. CCT only allocates its budget to cover the gaps to maintain public services as required.

This, on the one hand, helped reduce the government’s budget allocation to deliver public service. On the other hand, it may create inequality and compromise the accountability of PSDUs. New policies or initiatives are mainly dependent on central government transfers or unpredictable own-source revenue. The total expenditure of extrabudgetary funds is only around 1 percent of the total sub-national budget expenditure.

Efficient Use of Resources for Service Delivery

Efficiency gains are achieved in the use of resources for service delivery thanks to improvements in the procurement system and improved control of payrolls and non-salary expenditure. However, the variance in expenditure composition remains large. Neither annual nor in-year budget execution reports allow direct comparison between the original budget and expenditure outturns because of the carry-over practice and lack of economic classification in the presentation of budget plan. Transfers to district governments are mainly rules-based but not very timely. Resource allocation to some public service tasks, in particular public investment projects, is not sufficiently predictable.

Lack of performance information and incomplete and untimely public access to fiscal information are also impediments to the SNG and communities’ ability to monitor service delivery efficiency. The budget allocation and authorization to direct spending units are based on line items or inputs for tasks, which do not support the comparison of service performance with the actual resource received. The internal audit function is not yet in place and the feedback mechanism is reliant on the Inspectorate System. External audit is independent and regular to detect inefficiency in the public sector. The People’s Council uses audit reports for plenary hearings and its oversight missions but neither scrutinizes audit reports nor issues a scrutiny report and/or its own recommendations.

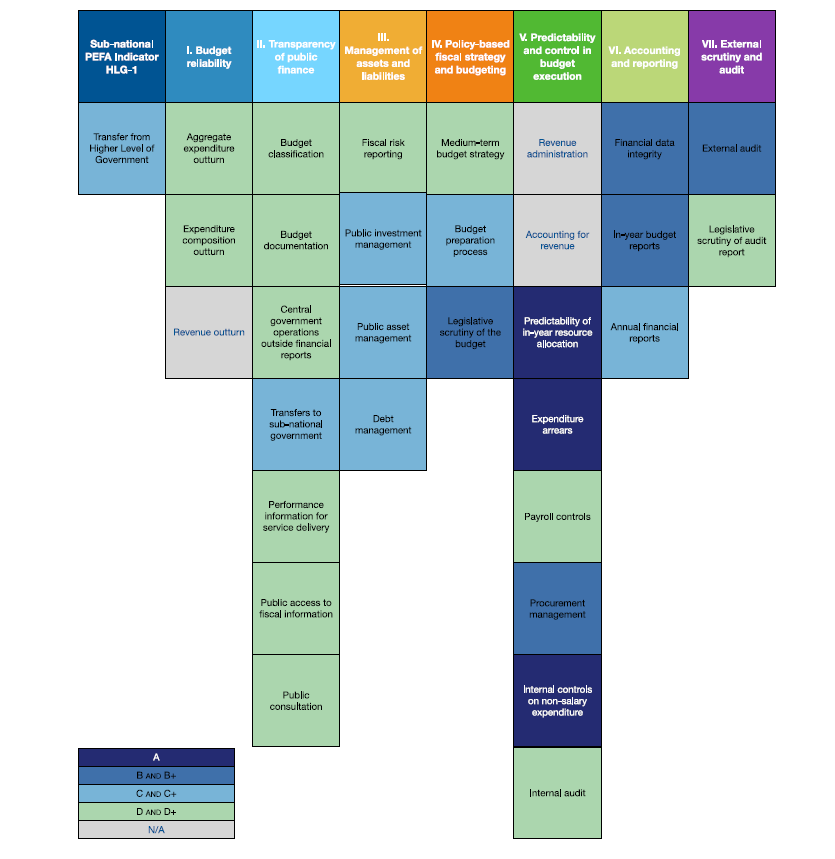

Figure 2: Summary of Overall PEFA Scores by Indicators