Mongolia Ulaanbaatar City 2022

Introduction

The assessment was undertaken jointly by the Government of Mongolia (GoM), the World Bank staff and consultants hired by the World Bank. The Ulaanbaatar City (UB City) of Mongolia played the lead role on the Government’s side, while the World Bank coordinated the assessment on behalf of the development partners. Development partners have reviewed the draft PEFA assessment and provided feedback on the quality of the review process as well as to the overall narrative. The core of the assessment oversight team included representatives of the World Bank who were responsible for undertaking the PEFA assessment and its quality assurance. The oversight team of the GoM was chaired by Mr. Sandagsuren. J, First Deputy Governor of Ulaanbaatar in charge of Economic Development and PPPs. UB City facilitated the provision of data and coordinated the reviews of the Concept Note and draft assessment report.

Methodology

The assessment is conducted according to the 2016 SNG PEFA Framework and used the Guidance for SNG PEFA Assessments issued by the PEFA Secretariat in 2022. The full set of SNG indicators has been applied according to the 2022 SNG framework (based on the 2016 PEFA methodology), including the SNG pillar on intergovernmental fiscal relations. The service delivery assessment module (the SD module) is applied in order to identify bottlenecks in service delivery due to PFM performance and thus inform efforts to improve service delivery in future.

Scope and coverage

This SNG PEFA assesses the PFM systems of UB City, primarily focused on the budgetary units of UB City. The existence and transparency of any extra budgetary operations are covered by PI-6 and such extrabudgetary units included within the scope of other indicators and dimensions according to the SNG PEFA framework. Public corporations, some of which receive financial support from UB City, are covered by PI-10 but are otherwise out of scope of the assessment. Nine districts within UB City are effectively separate levels of government, with their own governance and fiscal arrangements and therefore are not included within the set of budgetary and extrabudgetary units of UB city. Therefore, these lower-tier governments are not within the coverage of most indicators. However, the financial arrangements between UB City and districts are assessed by PI-7 and, because UB City funds service delivery by such entities, they are also included within the scope of PI-8.

Summary of Findings

A clear strength of the PFM system of UB City is the coverage of the budget and financial reporting, as both include the districts and the Publicly Owned Enterprises (POEs) as well as external sources of funding. This ensures a high degree of transparency of the policy choices and operations of UB City, and of the financial performance of associated entities. This helps to reduce the potential for unforeseen fiscal risks.

Another key strength is the robust nature of the collection and accounting for tax revenues, where the banking system and Treasury Single Account (TSA) structures are used to ensure timely recording of revenues. While much of this architecture belongs to the central treasury, its application in UB City adds to the transparency and efficiency of UB City’s operations and enhances the efficiency of its financial interactions with the CG.

This same central treasury architecture extends to processes for the release of recurrent funding and the operation of controls over the use of recurrent expenditure, which are generally robust. This is despite some reliance on manual processes (which impacts on efficiency rather than effectiveness of such controls). The introduction of the new electronic payroll system, which links to the HR system, is an example of how further use of technology solutions could improve internal controls over spending. Internal audit is in place for most of UB City. Overall, there is a reasonable degree of integrity of revenue as well as payroll and non-payroll expenditure data.

A further strength of the PFM system is the timely preparation of within year reports. Financial statements are prepared according to a stable set of accounting policies (although not yet IPSAS compliant). There is generally fast turnaround on audits of the annual financial statements, which are conducted according to international auditing standards. Similarly, there is timely completion of hearings regarding audit reports by the Citizen’s Representative Khural (CRKh).

On the downside, there has been large within-year shifts in the aggregate value and composition of revenue and expenditure during budget execution over the last three years that could not be readily explained. It is noted that there was some shifting in the nature of expenditure and revenue mandates and it is anticipated that these are driving some of these deviations in data – nonetheless, UB City should be capable of explaining these to readers of its key budget and reporting documents.

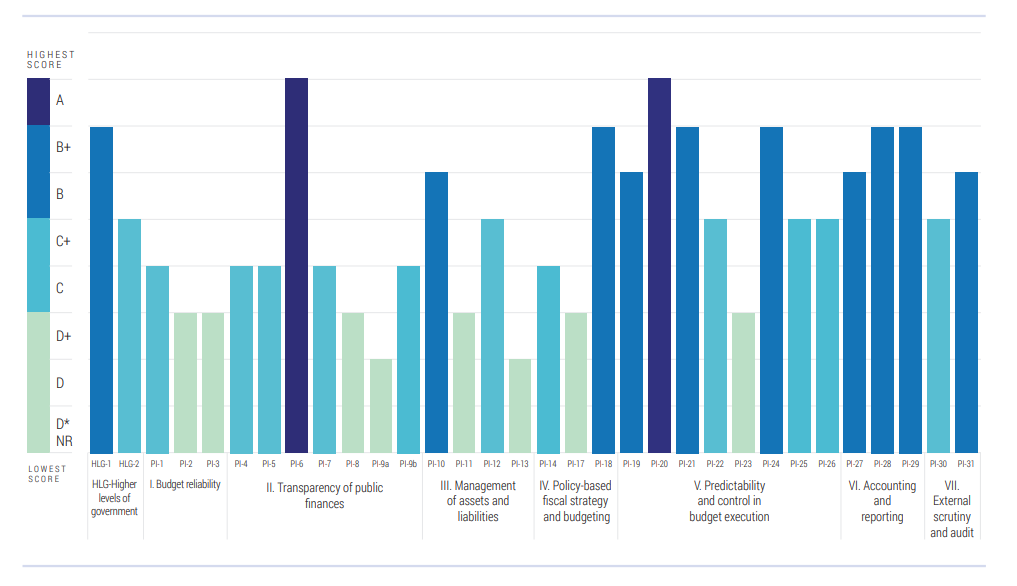

Summary of PEFA Scores by Indicators

Impact of PFM Performance on Budgetary and Fiscal Outcomes

Aggregate Fiscal Discipline

Over the last three years, UB City’s budget has not been a reliable indicator of actual fiscal outcomes. Both expenditure and revenue have deviated significantly from the original budget in aggregate and in terms of their composition. In 2021 UB City realized a large surplus, equivalent to around one third of its original budget. UB City’s budget has a single year focus, reflecting an historical approach of SNGs being funded each year only to deliver services to a standard determined by the CG (where planned surpluses are required to be transferred to CG). To the extent that there are unplanned retained earnings from under execution of the budget in the prior year, these are planned to be spent in the following year (effectively treated as revenue). Estimates of the fiscal impact of new policies and projects are costed for the budget year and the budget notes the total project cost but, consistent with the single-year approach, there is no breakdown of the annual costs of the project in future years. Recurrent costs of capital are not evident in the budget documents. The budget notes revenue policy changes and these are reflected in the overall revenue forecast but the precise impact of the policy (on a standalone basis) is not evident in the budget documents.

Strategic Allocation of Resources

There is a precisely defined approach by the CG to determine the level of funding required to fund services delivered by SNGs. Baseline levels of funding are determined based on precisely defined norms and standards for the required consumption of inputs based on historical reference points. As an example, a CG regulation determines the precise number of sheets of paper to be used by particular units. These funding norms were intended to define the level of financial support that was provided for specific purpose by the CG and to determine the level of resourcing that each aimag (or UB City) would require to deliver services at the mandated standard (norm) – with any shortfall covered by the CG and any surplus transferred to the CG.

This funding mechanism should be transparent but in recent years the CG deviated from its own standards in determining the largest of these special purpose transfers (SPTs) – this being the general education SPT.

This approach to funding also reflects a highly centralized, backward looking and control-oriented approach which, until some recent reforms in the health sector, provided very little flexibility for UB City to determine how it would utilize resources to achieve program goals. Such lack of flexibility is exacerbated by funding determinations by the CG being confirmed to UB City and its districts late in the budget process. As these SPTs are determined mainly on the norms[1]based funding of specific inputs to be consumed, performance targets in budget documents are essentially a list of planned activities rather than planned outcomes to be achieved by undertaking such activity.

UB City takes a very similar approach in relation to how it funds and manages its own Locally Owned Enterprises (LOEs) in their delivery of services. UB City tightly controls prices for such services (such as bus fares) and then subsidizes delivery in terms of specific funding per unit of activity. UB City then undertakes its performance management by taking an external measurement of the outputs produced, rather than the outcomes achieved, and then applying a financial penalty if outputs are not produced on time.

While UB City’s baseline budget is closely defined, it does have the ability to raise and spend revenue above the baseline and there is some discretion as to how capital expenditure is allocated. A new national approach to public investment management (PIM) has been implemented, supported by legislation, procedures and systems which is better at organizing PIM decision making. While this new PIM approach is not mandated for SNGs, UB City has adopted the methodology and there is evidence of this approach being used for prioritizing projects. However, the evidence of detailed economic assessment being completed is not available for the largest projects and it is not clear that UB City’s prioritization of projects is yet having the desired impact on the funding of capital projects.

UB City follows a consistent budget process that is well understood by participants but is not highly supportive of medium-term policy making. A clear budget circular is made available to internal budget governors and the districts which provides an opportunity for each to propose a budget for the coming year. There are some formal mechanisms for public consultation built into the budget process to assist UB City in prioritizing discretionary spending. However, as the timeframe for providing such submissions is short (around three weeks) and there are no ceilings, the submissions reflect a wish list of current and new spending rather than a prioritized set of new initiatives based on performance information and policy priorities.

The UB City budget cannot be submitted to the CRKh until the national budget is ratified and therefore the budget is not submitted to the CRKh until late November. The CRKh however has a defined scope and clear procedures for reviewing the budget and this enables the budget to be approved before the end of the year (typically in early December). Nonetheless, the timeframes for budget approval provides little time for districts and internal budget governors to adapt to changes in funding prior to the start of the year.

Efficient Use of Resources for Service Delivery

As outlined above, there is a precisely defined approach by the CG to determining the level of special purpose funding transferred to UB City and its districts for service delivery functions. This should be transparent but in some recent years the CG deviated from its own standards in determining the largest of these SPTs.

Once funding is allocated for service delivery functions, there is generally a high degree of predictability in the allocation of recurrent budget resources. All available cash resides in the national treasury single account framework and a schedule is agreed for the release of budget funds on a monthly basis, which enables the budget governors of UB City to make firm spending plans for the month ahead. Capital budgets are allocated during the year on a more ad hoc basis according to the planned timing of obligations being incurred. It is understood that national treasury has implemented some tight controls over release of funds for discretionary spending, such as capital, and that this contributed to a large underspending of capital by UB City in 2021.

In relation of program delivery, the procurement system (www.tender.gov.mn) provides data on what has been procured, and the new procurement law, which mandates open competitive tendering, has resulted in the UB City favoring such methods. There is a broad range of information available to the participants and public regarding tendering processes and outcomes, including complaints mechanisms. However, these complaints mechanisms are led by the procuring entity and thus lack independence. In addition, there is no recording of expenditure commitments prior to (or just after) goods or services are procured – which would ensure that budgeted funds are set aside and available to meet the resulting obligations.

It is an observed concern of program managers that the norms and standards which are used to define the budget for service delivery units, as well as regulated prices for services, are many years out of date and this creates a situation where large changes to the budget are required during execution to address these budget shortcomings. The absence of a medium term approach to budgeting makes it difficult for UB City to manage major changes in program funding, design and/or delivery, as the most significant of these would take multiple years to manage.

Like the resource allocation decisions, performance continues to be planned and measured based on what activities are required to produce planned outputs rather than focusing on the outcomes hoped to be realized. The use of performance information to punish/financially penalize service providers, rather than as a tool to improve policy making, represents a lost opportunity for UB City. Nonetheless, the reforms introduced to the health sector which provide greater flexibility as to how the budget envelope for health is internally allocated, are a beacon that indicate a pathway toward a more policy focused approach to budget preparation.